No products in the basket.

Every time there is a budget in the UK, the wine industry awaits with bated breath the decision of the Chancellor on alcohol duty. In 2022 when this blogpost was initially written there was no official budget. However a mini budget announced by short-lived Chancellor, Kwasi Kwarteng, in Liz Truss’ short-lived government froze duty on wine. It could be said that that was one of the few good decisions of that budget. The subsequent Chancellor, Jeremy Hunt, soon scrapped that decision, clearly not understanding the reasons why wine duty should be cut or frozen. Let’s find out why it makes sense to cut wine duty.

As a reminder alcohol duty is, according to HM Revenue and Customs (HMRC) “a tax that is charged on alcohol produced or processed in the UK or brought into the UK for consumption.” You may not notice increases in duty directly as this tax is paid by your retailer when the wine leaves a bonded or customs-controlled warehouse to go onto their shop shelves or to be sent directly to their customers; it is incorporated into the price that you pay. And we all know how wine prices, like everything else, have been rising in recent years.

Duty on wine has long been charged at different rates according to the type of wine and according to alcoholic strength. In 2022 £2.23 of the price of a bottle of still wine between 5.5% ABV and 15% ABV was duty. That excluded value added tax (“VAT”) incurred on the excise duty which took the total duty up to £2.68. And don’t forget of course the VAT of 20% on the bottle of wine itself. The excise duty rate – £2.23 on still wine and £2.86 on a bottle of sparkling wine – was regardless of whether the bottle of wine cost you £5 or £50.

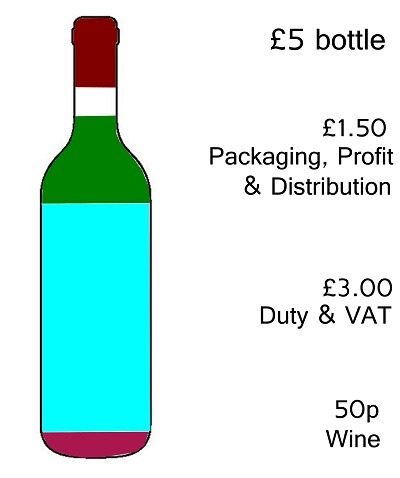

This by the way is one of the reasons why the starting price of my wines with attitude is around £15. For a £5 bottle of wine (in 2022), £3 or 61% is made up of duty and VAT whereas ‘only’ 31.5% or £4.73 of a £15 bottle of wine went to the government. But don’t get me started on the subject of cheap wine, let’s get back to the government’s penchant for increasing duty on wine.

The UK government’s policy paper on duty on alcohol then stated that all alcohol duty would rise by the Retail Price Index every year. This meant that in Jeremy Hunt’s first Budget the wine industry was expecting the Chancellor to raise those rates of duty by about 12.6% (Sept 22’s RPI rate) to £2.51 for still wine and £3.22 for a bottle of sparkling wine, ignoring VAT. Gulp!

You might think that a rise in line with inflation is fair – there was (and still is) a huge deficit to sort out after all – however there are a number of things to bear in mind…

We already pay rates of duty that are way higher than most EU countries. Although we are no longer in the EU, a comparison with 27 other countries is worth making. The level of excise duty payable on wine is set locally in each EU country; the EU just sets a “harmonised minimum rate” of alcohol duty for wine. That harmonised minimum rate for still and sparkling wine however is… €0, yes €0. So each country is free to choose what it charges and many countries choose not to charge any duty at all on wine (though the EU is reviewing its current practices).

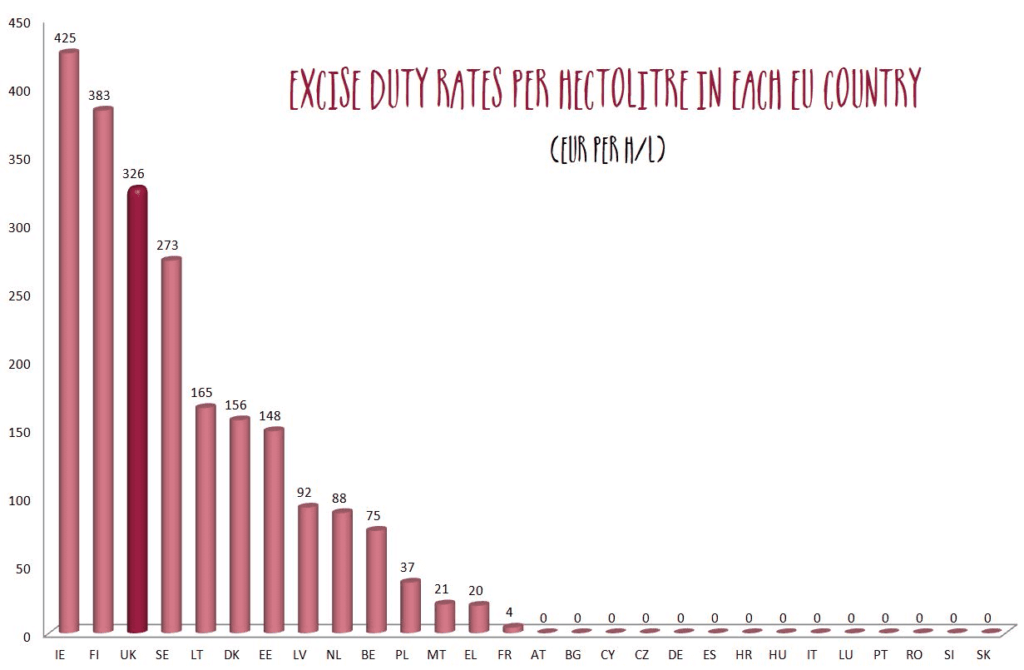

In the chart below produced from 2018 rates per hectolitre (in Euros according to the European Commission Excise Duty tables) you can see that 14 of the then 28 EU members did not charge excise duty on wine; in 2020 it was 15 of 27. Some of those that do charge excise duty only apply the charge to sparkling wine. If we compare the UK with EU countries, the UK pays one of the highest rates, the third highest rate after Ireland and Finland. The top 4 countries including the UK paid over €100 more per hectolitre than each of the rest of the excise duty paying countries; in the UK in 2018 we paid about £1.10 more in duty per bottle of still wine than Lithuania and about £2.42 more per bottle than France.

Duty on wine in the UK rose by an average of almost 6% p.a between 1987 and 2021 whereas the annual rate of inflation averaged 3.3% over the same period. It doesn’t seem quite fair somehow does it? 2008 was the worst year for wine lovers – the rate of duty rose 9% in March and then 8% in December. 12.6% seems a lot to stomach in one go.

To make matters worse the value of the pound declined by almost 21% over the same 35-year period. Events like Brexit, Covid-19 and the war in Ukraine have all contributed to sterling’s recent acute devaluation with the rising costs of holidays abroad and of imported goods being felt by all.

At the same time that excise rates escalated and we receive fewer Euros or US dollars for our pounds, inflation has been rising and most recently at an alarming rate so we have a triple whammy.

Health is cited as one of the main reasons for the high rates of tax on alcohol and there is no denying that it makes sense to support the health services required for alcohol-related illnesses. Whilst much is made about high levels of duty being a much-needed means to reduce alcohol consumption in the UK, there is as much evidence to suggest that the two are not directly linked as there is evidence to the contrary. Nor do health concerns explain why increases in duty on wine seem to be excessive when compared with rises in the rates applicable to beer and spirits. Organisations lobbying for increased rates of duty on alcohol or minimum unit prices like Alcohol Change UK acknowledge that inconsistent duty across the different categories of alcohol just creates a market for “cheap, high-strength products which do most damage to health.”

When the Government has frozen duty rates on alcohol, usually after much lobbying from the industry, there is evidence that revenue from wine duty in the UK grows. The Wine & Spirit Trade Association say that they have independent analysis “set out in a report we had commissioned, showing that the boost in economic activity if duty were frozen again would leave the wider economy better off, at no cost to the Treasury”.

In the first six months of 2019 wine duty receipts fell by 2.1% according to HMRC’s Alcohol Bulletin, a decrease of £51m after an increase in the rate of duty on wine. In the same period taxes from beer and spirits, upon which duty rates were frozen, rose exponentially.

Of course I haven’t mentioned yet the changes to the way in which duty is calculated since February 2023. At that point we moved to a system in which duty is paid according to the alcohol content (ABV) of alcoholic drinks. Whilst this is supposed to improve the current regime inherited from the EU, the huge difference in rates of duty to be paid per category does not seem very fair, especially to wine drinkers. Wine (and spirits) will be taxed more harshly than other categories: wine for example will be taxed at 26p per unit whereas cider will be taxed at only 9p per unit. Under the new system treasury receipts from duty on beer and cider will actually fall, whereas receipts from duty on wine will increase by £250m per annum.

The WSTA has long been campaigning for a reduction in the difference between the rates of different categories of alcohol, a position that Wines With Attitude fully endorses. But their efforts are repeatedly falling on deaf ears.

The duty system has long been burdensome but the changes since February 2023 are complex and, instead of improving things, are much more difficult and time-consuming to administer, impractical and costly.

I wrote in 2022 that if the Chancellor stuck to his plans, increases in alcohol duty were inevitable and the system more complex. This is an added burden for wine retailers especially in the November Budgets because the run up to Christmas accounts for a high percentage of sales. It feels like a tax on Christmas for us all. Bah humbug!

A continuation of the freeze on wine duty would certainly help the wider industry at a time when wine sales are in decline – certainly in volume terms – and we are all aware that pubs and restaurants across Britain are closing down every week. In my view the government also needs to have a re-think on duty in order to show support for UK wine makers as the market for English and Welsh wine grows, helped by vast improvements in recent years in quality. How can it be that a bottle of English sparkling wine bought in England incurs £2.86 excise duty but if purchased in Spain would incur no excise duty at all?

For an update on duty, part 2 if you like, take a look at my update duty blogpost.

It seems that now before every budget, letters are written to the Chancellor, pleas made via X and lots of fingers are crossed but always in vain. Treasury seems to think that wine drinkers are cash cows and have no limits. Sadly that is not the case. So if a cut in duty is out of the question, is it too much to ask for a freeze at the next budget?

© 2014-2026 Wines with Attitude Ltd | VAT Reg. No. 181 2419 22 | Registered in England 08918466 | Fiveways, 57-59 Hatfield Road, Potters Bar, Herts, EN6 1HS